On the Daily

On the Daily

ECB maintains a "transitory" view on inflation

Welcome to the FXDD Research: On the Daily newsletter. This publication provides readers with a sliver of our research process to help contextualize daily economic and market developments across the globe. We designed FXDD’s research process to be intuitive and actionable; therefore, you can expect regular call-outs on risk-reward scenarios we think are lucrative. We typically follow global macro markets, particularly the US, UK, EU, Japan, China, alongside the aggregate World economy. We also follow global assets, i.e., stocks, currencies, commodities, and fixed income (though to a lesser extent). We quantitatively do all this; therefore, you can expect most of our analysis to be standardized, consistent, and repeatable. Finally, while we will offer some call-outs and trading signals, we reserve our most granular work for our clients, so if you like what you see, please head over to our website (click here)to gain access to the arsenal of tools we have built.

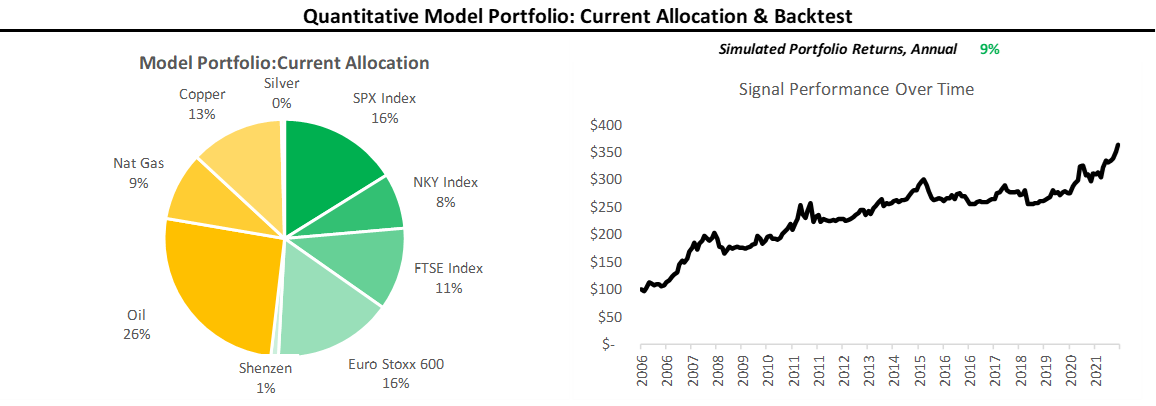

Before we dive into our updates, here’s a sneak peek into our quantitative portfolio allocation model. Our model allocated exceptionally well over the last month and has been up considerably due to its allocations to risk-on assets:

This morning, our portfolio strategy was down 0.8%, somewhat mitigating yesterday’s down day, taking the one-month rolling performance to 3.8%. We continue to think the quantitative process is well-allocated to the current market trend, i.e., INFLATION. Here are the most recent developments in global macro:

Global Economic Momentum: In the US, we had significant data out in the form of Initial Jobless Claims, which surprised to the upside, and Q3 GDP data, which surprised to the downside on a QoQ basis. Aside from the US data, we saw Japanese retail sales come in stronger than expected, though it provided no respite to the Nikkei which remains in a strong downtrend relative to other equity markets, reflecting Japan’s poor economic performance coming out of the COVID-19 pandemic.

Global Policy: The ECB announced its monetary policy decisions, and as expected, there were no significant changes to its policy implementation. The vast majority of the market’s focus has been on the uptrend in short-term rates in the Eurozone, and how the ECB will interpret this. During this meeting, the ECB has chosen to forgo dissuading markets from pricing higher interest rates (read: pricing higher inflation). We think this largely comes from uncertainty emanating from the ECB on the economic and inflation outlook. However, Lagarde continues to remain in the camp that views current inflation as transitory, which we don’t think is totally unfounded. Our models point to heightened inflation over the next few months (with decelerating rates in 2022), fairly consistent with the ECB outlook. We think the outcome of this meeting sets us up for an interesting meeting in December. While it is clear that the majority of the ECB interprets current inflation as transitory, there is enough doubt in the MPC that they have not gone far enough to impose it on markets through their speech. This hesitancy could extend itself into decision on the future of the ECB’s Asset Purchase Program (APP), making the package smaller than previously expected.

Global Market Trends: Today was yet another risk-off day after an extraordinary week for risk-on exposures last week. We continue to think that the high growth and inflation levels globally, alongside sustained monetary policy support from the BOJ, ECB, and Fed, will support inflationary and expansionary assets. However, given the receding acceleration in growth rates, it is worth thinking about the possibility of global stagflation. The bellwether of global stagflation is gold, which has picked up some momentum over the last few weeks. However, when we look at the cross-asset picture, there aren’t too many indications of a risk-off environment, i.e., where global bonds receive some amount of support. Further, our Trading Tools Report shows that gold offers an opportunity that is asymmetric to the downside, i.e., more conducive to a short position than a long position. Overall, we continue to think reflation will continue to run.

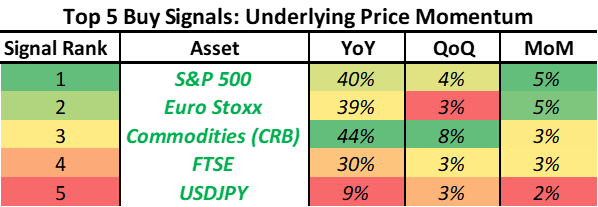

Having addressed the significant changes over the last 24 hours, let us look at our monitors and models. For those of you wishing to get “to the point,” here are our top trend signals on the long side:

Now, for those looking for more detail, let us look at the underlying models. We start by tracking economic data relative to consensus expectations, as the impact of financial data on markets depends on whether its surprises the upside or downside. We standardize this data and call this indicator Economic Momentum, i.e., higher values are positive and lower values are negative. The color-coding in the table represents higher/more downward momentum for a given country:

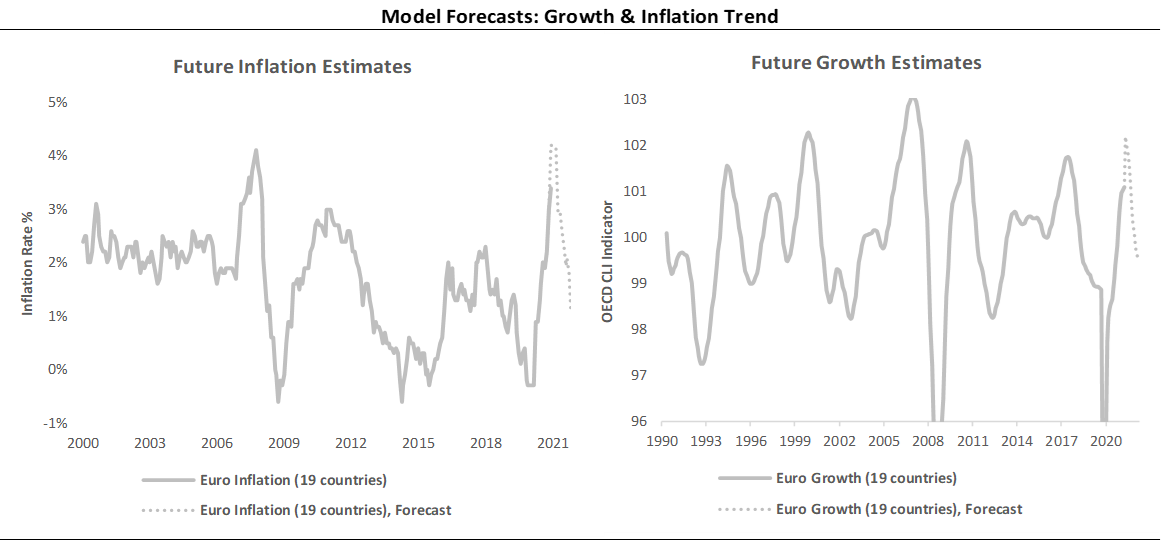

Next, we show our estimates for growth through the lenses of our forecasts for Euro Area growth & CPI indices from the OECD. Particularly, we highlight the fact that our models imply sustained levels of inflation in the near term, with moderating acceleration as we head in 2022:

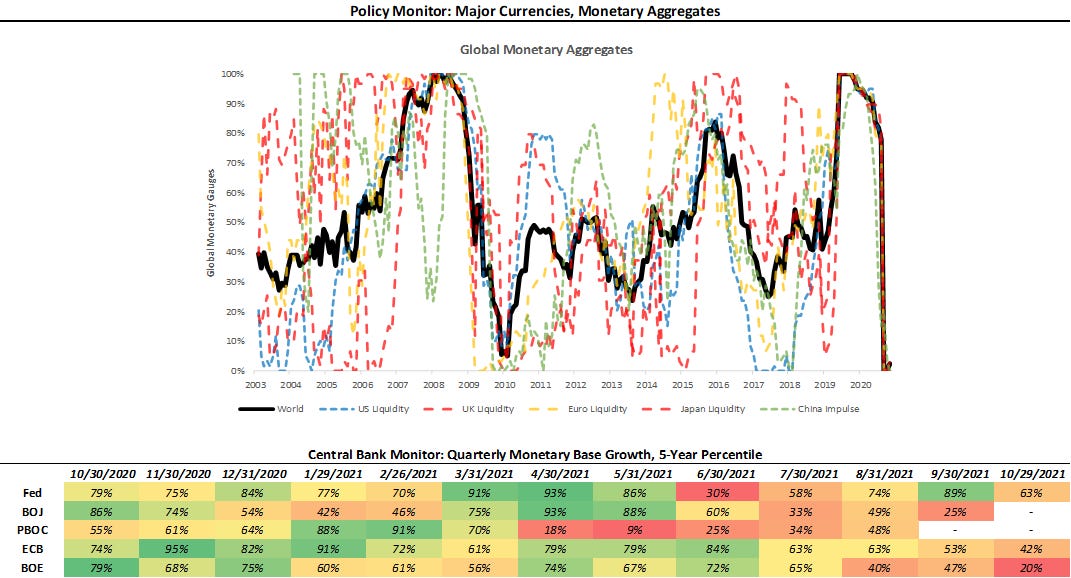

Next, we show our Global Policy Monitor, which tracks the broadest measures of private-sector monetary aggregates (M4 money supply, credit impulse, etc.) along with our tracking of effective-central bank balance sheets (monetary base). The measures are normalized and standardized, with values above 50 implying rising monetary aggregates and below 50 reflecting slowing growth. The color-coding reflects increasing monetary base relative to its 5-year history for a given country:

Next, we turn to how this combination of policy and economics reflects in markets. Below, we show our Market Trend Monitor, which tracks changes in global investment markets to classify market pricing as expansionary, inflationary, deflationary, or stagflationary. We typically prefer allocations in line with the current market trend. The current market trend is INFLATION, i.e., favoring commodities:

Next, we look at our Currency Bloc Monitor, which aggregates exchange rate moves across 20+ currency pairs into significant regions or Blocs. We use this method to estimate the flow of capital in the global economy. The color-coding in the table reflects the strength of a Currency Bloc versus others for a given time frame. We show the evolution of these Currency Blocs over time:

Finally, we show our Trading Tools Report, for the Nikkei, given the recent BOJ policy changes. We display our various screens to assess risk and reward:

We look forward to sharing our extensive library of content with you over the months to come. If you enjoyed these materials, feel free to share this with friends or colleagues, and don’t forget to subscribe for more!

Disclaimer: 75% of Retail Client accounts lose money when trading CFDs with FXDD Malta. You should consider whether you can afford to take the high risk of losing your money.